Hard Money Foreclosure Financing

Table of Contents: Hard Money Foreclosure Financing for Credit Challenged Borrowers in 2025!

- I. Introduction: Navigating 2025’s Foreclosure Landscape with Hard Money

- II. Hard Money Loans Unveiled: Your Strategic Edge in Real Estate Investing

- Key Distinctions from Traditional Financing

- III. The Nuances of Hard Money: Interest Rates, LTV, and Lender Risk Mitigation

- Understanding Higher Interest Rates

- Navigating Loan-to-Value (LTV) Ratios

- Understanding Points and Fees

- IV. Empowering the Credit-Challenged: Why Hard Money Loans Are Your Ally

- Property Value Over Credit Scores

- Specific Scenarios for Credit-Challenged Borrowers

- Dispelling Common Misconceptions

- V. Mastering the “Quick Flip”: Hard Money for Maximum Profit Potential

- The Foreclosure, Bank REO and Distressed Real Estate Properties Fix-and-Flip Strategy Defined

- The Critical Role of Speed

- Maximizing ROI with Hard Money

- VI. 2025 Market Insights: Trends Shaping Hard Money Foreclosure Financing

- Foreclosure Market Outlook for 2025

- Emerging Trends in Private Lending

- Regulatory Landscape in 2025

- VII. Your Blueprint for Success: Securing and Maximizing Your Hard Money Loan

- Essential Borrower Requirements and Preparation

- The Importance of a Clear Exit Strategy and Property Due Diligence

- Guidance on Choosing a Reputable Hard Money Lender

- VIII. Ready to Capitalize on Opportunity?

Hard Money Foreclosure Financing for Credit Challenged Borrowers!

I. Introduction: Navigating 2025’s Foreclosure Landscape with Hard Money

The real estate market in 2025 presents a dynamic landscape for investors. Data from April 2025 indicates a continued annual increase in U.S. foreclosure activity, with filings up 13.9% from the previous year and foreclosure starts rising 16.1% year-over-year. While these figures suggest a gradual escalation in distressed properties, it is important to note that overall volumes remain below historical norms, indicating that the market is not experiencing a broad collapse comparable to 2008. This nuanced environment, characterized by an increasing supply of distressed properties without catastrophic market depreciation, creates a unique and opportune setting for investors. This particular market condition, stemming from a return to more typical foreclosure levels after the pandemic-era moratoriums, coupled with robust homeowner equity, provides more inventory for investors while reducing systemic risk, thereby enhancing the appeal and stability of the “quick flip” strategy.

Concurrently, the traditional lending sector faces significant challenges. Mortgage applications declined by 6.2% in early 2025, with refinances falling by 13% compared to the previous year, making conventional financing increasingly difficult to secure. Banks are reportedly denying 43% of commercial loan applications as of Q1 2025, and mortgage rates continue to hover around 6.7%. This tightening of traditional credit creates a substantial gap in the market. This scenario elevates hard money loans beyond being merely an alternative; they are becoming a primary, strategic necessity for investors who require swift capital or whose financial profiles do not align with conventional lending criteria. For individuals who are self-employed or possess complex financial structures, the stricter traditional lending standards directly drive an increased demand for hard money, positioning it as a vital solution rather than a niche product.

In this evolving market, hard money loans emerge as a strategic solution. These are short-term, asset-based loans provided by private lenders, secured by real property, and renowned for their rapid funding capabilities. They are particularly valuable for real estate investors, especially those focused on “fix-and-flip” projects or the acquisition of distressed properties. Crucially, for credit-challenged borrowers, hard money loans offer a viable path to financing, as lenders prioritize the property’s intrinsic value over the borrower’s credit history.

II. Hard Money Loans Unveiled: Your Strategic Edge in Real Estate Investing

Hard money loans represent a distinct category of financing, fundamentally different from traditional mortgages. They are characterized as asset-based financing, meaning the loan is secured primarily by the real property itself, rather than solely relying on the borrower’s creditworthiness or financial profile. This foundational distinction is what facilitates their notably faster underwriting and approval processes. Typically, these loans are short-term, with durations often ranging from 6 to 18 months, though some can extend to 24 or even 36 months for more extensive rehabilitation projects. Their repayment terms are considerably shorter than the conventional 15- or 30-year mortgages. Funding for hard money loans usually originates from private lenders or investor groups, not traditional banks , a factor that significantly contributes to their speed and flexibility.

Key Distinctions from Traditional Financing vs. Hard Money Foreclosure Financing

The advantages of hard money loans become particularly evident when contrasted with conventional financing options:

- Speed: Hard money loans close at an accelerated pace, frequently within 5-10 business days, a stark contrast to the 30-60 days typically required for traditional mortgages. This rapid turnaround is paramount for time-sensitive real estate transactions, such as foreclosures or properties acquired at auction. The swift funding capability of hard money loans allows investors to present offers that are nearly as compelling as cash transactions, significantly enhancing their ability to secure high-potential properties that might otherwise be missed through slower, traditional financing routes. This capacity provides a critical competitive advantage in dynamic markets.

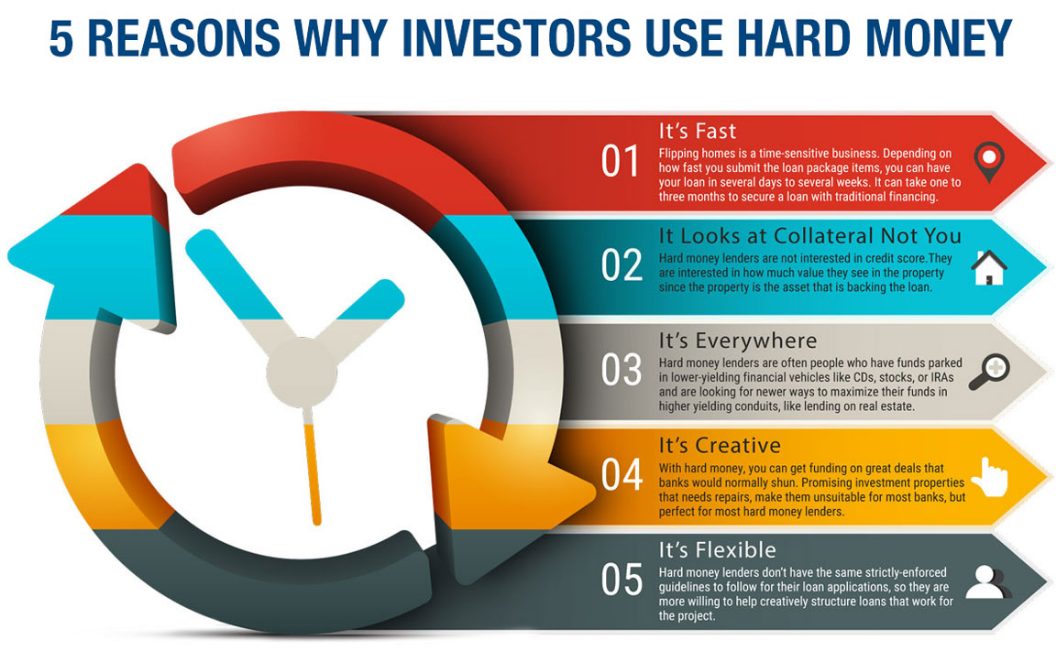

- Approval Metrics: Hard money lenders primarily assess the property’s value and its projected potential, specifically its After-Repair Value (ARV), rather than adhering to stringent credit scores, debt-to-income ratios, or requiring extensive income documentation. While lenders may still review credit reports, their ultimate underwriting decisions are fundamentally based on the tangible asset, enabling loan approvals even for individuals with FICO scores in the low 400s.

- Loan Purpose: Unlike traditional loans, which are typically designed for primary residences or long-term investments, hard money is optimally suited for specific, strategic purposes, including fix-and-flip projects, bridge financing, and the acquisition of distressed assets.

While hard money loans have historically been perceived as “loans of last resort” , the current market environment and their inherent characteristics demonstrate a clear evolution. The overwhelming evidence from various sources indicates their strategic utility for experienced investors who prioritize speed, flexibility, and the ability to capitalize on unique opportunities. This shift in perception reflects a maturing market where investors increasingly recognize the distinct value of hard money for specific, high-ROI strategies, moving beyond viewing it solely as a desperate measure for those unable to secure traditional bank financing.

III. The Nuances of Hard Money Foreclosure Financing: Interest Rates, LTV, and Lender Risk Mitigation

Understanding the specific financial characteristics of hard money loans is crucial for effective investment planning. These loans come with particular nuances regarding interest rates and loan-to-value (LTV) ratios, which are intrinsically linked to how lenders manage risk.

Understanding Higher Interest Rates for Hard Money Foreclosure Financing

Hard money loans generally carry higher interest rates compared to conventional mortgages. This higher cost is a direct consequence of the increased risk assumed by lenders, who prioritize the property’s value over the borrower’s credit history and provide significantly faster funding with less stringent documentation. In 2025, first-position hard money loan interest rates typically range from 9.5-12%, with some sources indicating a broader range of 8-15%. Second-position loans may see rates from 12-14%. Various factors influence these rates, including the borrower’s credit (though less critical than for traditional loans), the property’s condition and location, the requested LTV ratio, and the lender’s overall assessment of the loan scenario’s perceived risk.

It is important to view these higher interest rates and associated fees not as inherent disadvantages, but as a calculated cost of doing business. This cost is directly justified by the unparalleled speed and flexibility that hard money offers, enabling investors to seize time-sensitive, high-ROI opportunities that would be inaccessible through traditional financing. As some market observers note, for time-sensitive transactions, the speed and flexibility of hard money often outweigh the additional interest.

Navigating Loan-to-Value (LTV) Ratios for Hard Money Foreclosure Financing

The concept of Loan-to-Value (LTV) in hard money lending requires careful consideration. While the perception might be of “lower LTV,” the reality is more nuanced. Hard money lenders mitigate their risk by not financing 100% of a property’s value, thereby ensuring an equity cushion. However, when applied to distressed properties, hard money LTVs can be considered advantageous because they are frequently based on the After-Repair Value (ARV) rather than solely the current purchase price. This approach allows lenders to offer financing up to 70-90% of the ARV or 85-90% of the purchase price , enabling investors to secure more capital for both the acquisition and the necessary rehabilitation.

Lenders typically require a substantial down payment, often ranging from 10-30% or more, which is considerably higher than the 3% down payment sometimes seen with conventional loans. This “skin in the game” from the borrower further reduces the lender’s risk. This dynamic means that while a “lower LTV” from a lender’s risk perspective ensures a safety margin, it simultaneously translates to a “high LTV” from a borrower’s leverage perspective on a distressed asset, particularly when considering the ARV. This structure is a powerful form of leverage for fix-and-flip investors.

Understanding Points and Fees for Hard Money Foreclosure Financing

Beyond interest rates, hard money loans often include additional costs such as origination points, typically 1-2%, and various other fees. These fees contribute to the overall cost of the loan and must be meticulously factored into the investment’s profitability calculations. It is also important for borrowers to be aware that some lenders may impose prepayment penalties, which should be explicitly disclosed in the loan commitment and documents.

To provide a clear overview, the following table highlights the key differences between hard money loans and traditional financing:

| Feature | Hard Money Loan | Conventional Loan |

| Approval Speed | 5-10 days | 30-60 days |

| Primary Focus | Property Value/ARV | Credit Score, Income, DTI |

| LTV Ratios | Up to 70-90% of ARV | Up to 80% of purchase price |

| Interest Rates | 8-15% | 3-7% (historical/lower) |

| Points/Fees | 1-2% origination | 0.5-1% |

| Loan Term | 6-24 months | 15-30 years |

| Funding Source | Private Lenders/Investors | Banks/Mortgage Companies |

| Down Payment | 10-30% | Typically 3-20% |

| Ideal Use Cases | Fix-and-Flip, Bridge, Distressed Assets | Primary Residence, Refinance |

This comparative table offers a concise, side-by-side analysis, immediately highlighting the unique advantages and disadvantages of hard money loans. For investors, this visual summary facilitates a rapid understanding of how hard money integrates into their financing strategy. It directly addresses the need to detail the nuances by contrasting them with traditional options, making complex financial information digestible and reinforcing the strategic nature of hard money.

IV. Empowering the Credit-Challenged: Why Hard Money Foreclosure Financing Loans Are Your Ally

For individuals and investors facing credit challenges, hard money loans offer a powerful and often essential pathway to real estate opportunities. Their fundamental structure prioritizes tangible assets over traditional credit metrics, thereby leveling the playing field for many.

Property Value Over Credit Scores for Hard Money Foreclosure Financing

The distinguishing characteristic of hard money loans is their asset-based nature, where the property’s intrinsic value and its potential for appreciation or renovation serve as the primary collateral, rather than the borrower’s credit history. This fundamental difference makes them highly accessible for individuals with less-than-perfect credit. While hard money lenders may still review credit reports, their underwriting decisions are predominantly based on the “hard assets”—the real estate itself. This allows for loans to be approved and closed even for borrowers with FICO scores in the low 400s. This emphasis on property value over credit score democratizes access to real estate investment for segments of the population traditionally underserved by conventional banks. It enables a wider range of individuals, including the self-employed, those with past credit issues, or even new investors without extensive credit history, to participate in the real estate market, fostering broader economic participation and wealth creation beyond the traditional financial gatekeepers.

Specific Scenarios for Hard Money Foreclosure Financing for Credit-Challenged Borrowers

Hard Money Foreclosure Financing as Hard Money Loans prove particularly beneficial in several specific scenarios for borrowers with less-than-perfect credit:

- Homeowners Facing Foreclosure with Substantial Equity: For homeowners struggling with mortgage payments but possessing significant equity in their property, a hard money loan can provide rapid access to capital. This quick infusion of funds can be used to stave off foreclosure, allowing the homeowner to sell the property on their own terms, preserving their equity, or to resolve the underlying financial issues. In this context, hard money loans function as a rapid bridge, enabling these homeowners to leverage their existing equity to avoid losing it entirely, thereby providing a vital lifeline for individuals in distress and offering a path to financial recovery or a more controlled sale.

- Self-Employed Individuals: Many self-employed individuals strategically utilize tax write-offs, which can make it challenging to demonstrate sufficient income for traditional mortgage qualification, even if they have ample cash flow. Hard money loans offer a viable alternative in such situations, where their tax returns may not accurately reflect their true financial capacity.

- Investors with Past Financial Setbacks: Even with a challenging credit history, a well-articulated plan for property renovation and resale, combined with a robust exit strategy, can be sufficient to secure funding from hard money lenders.

Dispelling Common Misconceptions for Hard Money Foreclosure Financing

It is important to dispel certain common misconceptions surrounding hard money loans. One prevalent myth is that these loans are exclusively for investors with poor credit. While they certainly provide accessibility for this group, many experienced investors with excellent credit strategically utilize hard money loans for their speed and flexibility in time-sensitive deals. Another misconception is that the application process for hard money loans is overly complicated; in reality, it is often simpler and requires less documentation than traditional bank financing.

V. Mastering the “Quick Flip”: Hard Money for Maximum Profit Potential

The “quick flip” strategy is a cornerstone of many real estate investment portfolios, and hard money loans are uniquely suited to maximize its profit potential.

The Fix-and-Flip Strategy Defined utilizing Hard Money Foreclosure Financing

A fix-and-flip loan is a short-term financing solution specifically designed to assist investors in acquiring distressed properties, undertaking necessary renovations, and then rapidly reselling them for a profit. The core objectives of this strategy are to minimize renovation expenses, maximize the property’s market value post-rehab, and execute the sale as quickly as possible. The typical timeframe for completing a successful flip project, often ranging from 6 to 9 months, aligns seamlessly with the characteristic short terms of hard money loans.

The Critical Role of Speed in Successful Hard Money Foreclosure Financing

The speed at which hard money loans provide capital is not merely a convenience; it is a fundamental driver of profitability in the fix-and-flip model. Hard money lenders can deliver funds in a matter of days, providing investors a significant competitive advantage over buyers who are reliant on the protracted processes of traditional lenders. This rapid funding capability is absolutely paramount when acquiring distressed properties, which frequently come with tight deadlines, such as auction sales or pre-foreclosure opportunities. The ability to close deals swiftly enables investors to secure properties before competitors utilizing slower, conventional financing methods. The rapid approval and funding of hard money loans directly impact the profitability of a flip. The quicker an investor can acquire a distressed property, commence renovations, and reintroduce it to the market, the lower their holding costs (such as interest, taxes, and insurance) and the faster their capital is released for subsequent projects. This acceleration of capital velocity allows for the completion of multiple flips within a single year, significantly amplifying annual Return on Investment (ROI).

Maximizing ROI with Hard Money Foreclosure Financing

Hard money loans are structured to facilitate maximum ROI in fix-and-flip scenarios. They can cover a substantial portion of the purchase price and frequently extend to cover 100% of rehabilitation expenses, thereby preserving the investor’s personal capital for other investments or unforeseen contingencies. In 2025, the average gross profit for house flips stands at $73,500, with an impressive average ROI of 30.4%. The countrywide average success rate for house flips is reported at 88%.

Consider a practical example: An investor intends to flip a property purchased for $250,000, planning $75,000 in renovations, with an anticipated resale value of $400,000. A conventional bank might only offer a 65% LTV on the initial purchase price. In contrast, a hard money solution could provide 80% LTV of the $400,000 After-Repair Value (ARV), amounting to $320,000, plus 100% of the $75,000 rehab costs, totaling $395,000 in funding. This enables the investor to close the deal in just 7 days, complete the rehab in 5 months, and sell the property for $410,000, realizing a $35,000 profit after expenses. This illustration underscores how the unique structure of hard money loans—particularly their ARV-based lending and comprehensive rehab financing—directly enables highly profitable flipping ventures.

By enabling the swift acquisition of foreclosures and other distressed assets, hard money loans play a pivotal role in expediting the return of these properties to productive use. This not only benefits the individual investor but also contributes to the broader housing market by reducing the inventory of dilapidated homes and fostering neighborhood revitalization. This demonstrates that hard money lending, while driven by profit motives, also serves a wider economic function in maintaining market liquidity and property value stability, especially within segments impacted by foreclosures.

VI. 2025 Market Insights: Trends Shaping Hard Money Foreclosure Financing

The landscape of hard money lending in 2025 is being shaped by dynamic market conditions and evolving regulatory frameworks. A comprehensive understanding of these trends is essential for investors seeking to leverage hard money for foreclosure financing.

Foreclosure Market Outlook for 2025 Utilizing Hard Money Foreclosure Financing

As previously noted, foreclosure activity in 2025 is experiencing a gradual increase, with both foreclosure starts and completions showing annual gains. However, it is crucial to recognize that overall volumes remain below historical norms and do not signal a housing market crash akin to 2008. A significant mitigating factor is the strong homeowner equity positions prevalent in many markets, which continue to buffer against a more substantial surge in foreclosures. This allows many homeowners facing financial difficulties to sell their homes and preserve their equity, rather than losing it to foreclosure. This environment creates a market where distressed properties are becoming more available, presenting viable opportunities for investors, all within a relatively stable overall market context.

Emerging Trends in Private Lending for Hard Money Foreclosure Financing

The private lending sector, including hard money, is undergoing significant transformation:

- Increased Demand: With conventional lenders imposing stricter credit requirements and traditional mortgage applications declining, the demand for hard money loans is projected to rise throughout 2025.

- Private Credit Growth: The global private credit market has expanded by 15% to reach $3.5 trillion, indicating ample liquidity for non-bank lenders. This market is anticipated to grow to $2 trillion in assets by 2025, with major alternative asset managers investing billions. This substantial influx of capital translates into increased competition among lenders and a wider array of choices for borrowers.

- Technological Advancements: 2025 is witnessing a revolution in private lending driven by AI-driven underwriting, virtual staging and tours, and advanced digital platforms. AI and data analytics are reducing approval times and enhancing the accuracy of risk assessments by up to 40%. Online platforms are streamlining the lending experience, enabling brokers to monitor deals and exchange documents efficiently. For investors, these technological advancements offer a direct competitive advantage, as lenders leveraging these tools can provide even faster turnarounds, allowing investors to seize opportunities, such as foreclosures, with unprecedented speed and certainty, thereby maximizing their efficiency and ROI.

- Increased Competition: The growing number of private lenders entering the market means borrowers have more options and should actively seek the most favorable terms.

- Bridge Financing: Amidst rising interest rates, bridge loans are experiencing heightened demand as real estate investors seek short-term funding solutions to bridge the gap between property purchases and securing long-term financing.

- Hard Money Jumbo Loans: These specialized loans, which exceed conforming loan limits (typically over $726,200 in 2025), are gaining prominence for high-value, time-sensitive projects.

Regulatory Landscape in 2025 for Hard Money Foreclosure Financing

The hard money lending industry is also experiencing increased regulatory scrutiny, with a focus on tighter rules concerning disclosures and borrower protections. The Consumer Financial Protection Bureau (CFPB) has updated its thresholds for “high-cost mortgage loans” under Section 32 of Regulation Z, effective January 1, 2025. Loans that exceed these Annual Percentage Rate (APR) or points/fees thresholds now necessitate additional borrower safeguards, including mandatory pre-loan counseling and more stringent underwriting processes. Furthermore, various states are implementing stricter hard money lending rules, with some potentially introducing caps on interest rates and fees.

The convergence of increased private credit growth, widespread technological integration, and heightened regulatory scrutiny points to a significant trend: the professionalization and maturation of the hard money lending industry in 2025. This sector is moving away from a less regulated, “wild west” image towards a more sophisticated, tech-enabled, and compliant environment. While borrowers might encounter slightly more stringent disclosure requirements, they can anticipate a more transparent and potentially safer lending experience, which fosters greater trust in hard money as a legitimate and reliable financing option.

VII. Your Blueprint for Success: Securing and Maximizing Your Hard Money Foreclosure Financing

Successfully navigating the Hard Money Foreclosure Financing lending landscape requires careful preparation and strategic decision-making. While these loans offer unparalleled flexibility, a borrower’s approach can significantly impact their success.

Essential Borrower Requirements and Preparation

While hard money lenders place less emphasis on traditional credit history, they do meticulously assess other critical aspects of the borrower’s profile. Lenders evaluate the borrower’s experience in real estate, their overall financial stability, and, crucially, their proposed exit strategy for the property. Borrowers should be prepared to make a substantial down payment, typically ranging from 10-30% of the loan amount. A robust loan application should include clear documentation of income, assets, and liabilities, along with a well-prepared business plan that articulates the loan’s purpose and a detailed repayment strategy. Additionally, borrowers should anticipate the requirement for a professional appraisal, as many lenders use this to assess both the property’s current value and its After-Repair Value (ARV). While hard money lenders primarily focus on asset value, the importance of the borrower’s experience, financial stability, and exit strategy cannot be overstated. This indicates that borrower preparedness is not merely a formality but a critical component of risk mitigation for both the lender and the borrower. A well-prepared borrower reduces the lender’s risk of default and significantly increases the borrower’s likelihood of a successful, profitable project, thereby making the hard money loan a more effective tool for all parties involved.

The Importance of a Clear Exit Strategy and Property Due Diligence

A clearly defined exit strategy—whether through resale, refinancing, or generating rental income—is paramount for hard money loans to ensure timely repayment and prevent default. It is also prudent for borrowers to develop contingency plans in case market conditions shift unexpectedly.

Thorough due diligence on the prospective property is equally critical. This includes obtaining professional appraisals, conducting independent property inspections, and formulating conservative After-Repair Value (ARV) estimates that realistically account for current market conditions and comparable sales data. Furthermore, it is essential to factor in potential rehabilitation delays, unexpected costs, and market fluctuations into the project’s financial projections.

Guidance on Choosing a Reputable Hard Money Lender

Selecting the right hard money lender is a pivotal decision. Consider the following factors:

- Reputation and Experience: Prioritize lenders with a strong reputation and substantial experience within the industry. Reviewing online testimonials and ratings can provide valuable insights into other borrowers’ experiences.

- Loan Terms and Fees Transparency: Meticulously examine the interest rates, loan duration, and all associated costs—including origination fees, servicing charges, and potential penalties—upfront. Ensure a complete understanding of the repayment schedule and any applicable prepayment penalties. The increasing emphasis on transparent disclosures and borrower education, partly driven by regulatory scrutiny, means that lenders are increasingly obligated to clearly explain all costs and terms. This professionalization implies that borrowers can expect greater clarity, empowering them to make more informed decisions and fostering trust within the hard money market.

- Communication: Opt for lenders who maintain clear, consistent dialogue throughout the process and provide transparent breakdowns of all costs.

- Specialization: Some lenders specialize in specific types of hard money loans, such as residential or commercial projects. Choosing a lender whose expertise aligns with your investment type can be beneficial.

VIII. Ready to Capitalize on Opportunity?

The dynamic real estate market of 2025, particularly with its evolving foreclosure landscape, presents unique opportunities for astute investors. Hard money loans offer a powerful, flexible, and rapid financing solution, especially for those with credit challenges, enabling them to seize time-sensitive deals and maximize returns through strategic “quick flip” scenarios.

To explore how hard money financing can align with your investment goals and accelerate your path to profitability, we invite you to take the next step.

Request Your Complimentary Hard Money Consultation Today!

Connect with our network of pre-screened hard money lenders to:

- Benefit from quick turnaround times, which are essential for navigating competitive foreclosure and distressed property markets.

- Maximize your Return on Investment (ROI) by leveraging flexible financing solutions tailored for profitable “quick flip” scenarios.

- Access financing even with less-than-perfect credit, as our lenders focus on the inherent strength and potential of your property investment.

Hard Money Foreclosure Financing, Credit Challenged Hard Money Loans, Quick Flip Real Estate Financing, Distressed Property Hard Money, Hard Money Lenders Bad Credit, 2025 Hard Money Loan Trends, Foreclosure Property Investment Loans, Asset-Based Real Estate Loans, Fix and Flip Loans for Investors, Short-Term Real Estate Financing

Your Gateway to Distressed Real Estate Opportunities: NationalForeclosures.com

Navigating the landscape of Foreclosures, Bank REOs, and pre-foreclosures requires timely, accurate, and comprehensive data. NationalForeclosures.com is your premier resource for unlocking these hidden opportunities. Our robust databases compile detailed information on properties across all stages of distress, nationwide.

Whether you are a seasoned real estate investor looking for your next lucrative deal, a first-time buyer seeking an affordable home, or simply interested in understanding the distressed property market, our platform offers the tools you need.

- Single Property Information Data Purchase: For those with specific properties in mind or who prefer to test our data, you can purchase detailed information on individual properties. This includes vital details on the property’s status, estimated value, lender information, and key dates in the foreclosure timeline.

- Monthly Membership Access: For continuous access to a wealth of opportunities, our monthly membership provides access to a limited number of property information data per month. This allows you to consistently monitor new listings, track properties through their various stages of distress, and identify emerging opportunities in your target markets.

At NationalForeclosures.com, we empower you with the knowledge and resources to make informed decisions in the dynamic world of distressed real estate. Don’t miss out on these unique investment possibilities. Explore our membership options today and start uncovering your next property success story.

NationalForeclosures.com is owned & operated by NetBossMedia.com and is powered in part by: